With the deadline for filing annual income tax returns approaching – a reminder of applicable social security contributions and PIT after reaching the income threshold of 60 national monthly average salaries

We would like to remind you that in Lithuania from the moment the person’s income* reaches a certain threshold the taxes withheld from their salary change. This is according to the provisions of the Personal Income Tax law of the Republic of Lithuania and the State Social Insurance Law of the Republic of Lithuania which have entered into force as of January 1, 2019.

For 2024 and beyond, the threshold is set at 60 national monthly average salaries. This means that in 2024, the officially announced monthly average salary was equal to 1902,70 Eur, hence, the threshold for tax changes on the income received by the employee, was at the level of 114 162 Eur. In subsequent years, this threshold will increase depending on the national monthly average salary approved for that year (e. g..: in 2025, 60 national monthly average salaries will equal to 126 532,80 Eur).

It is important to highlight, that in the month in which the employee‘s income reaches the set threshold, the State Social Insurance contributions are recalculated – only the health insurance tax (6,98 %) remains to be paid by the employee, and the State Social Insurance contributions (12,52 %) as well as the additional pension accumulation (3 %) are no longer applicable for the rest of the year. Do note that the income threshold does not apply to employer contributions. Meanwhile, according to the Law on Personal Income Tax of the Republic of Lithuania, all income received by a taxpayer during the year that corresponds to an employment relationship or its essence (except sickness, maternity, paternity, childcare, and long-term work benefits), and exceeds the set income threshold is taxed with personal income tax (PIT) at a rate of 32 % instead of 20%.

The overpayment of the employee’s social security tax may be refunded to the employee in the same month after the necessary payroll corrections have been made internally, or with the next month's payroll. In the opinion of the tax authority, the refund of the overpaid social insurance tax should cover the additional 12 % of the PIT for the month in which the employee received income exceeding the set income threshold. Sodra informs all insurers (employers) that the employee has reached the income threshold and that the new tax rates apply. The employee is also informed via his personal account on the Sodra webpage. The employer can see the information on the changes in the Sodra report on the declared income per month, which indicates the month in which the contribution rates are changed and the amount of tax overpayment to be returned to the employee. It should be mentioned that if any prior month income recalculations are made, these contribution returns may be recalculated additionally.

Unlike with Social Insurance taxes, which are subject to mandatory changes by Sodra, the responsibility for paying a higher PIT rate lies with the taxpayer. This means that the higher PIT rate is not required to be applied during the monthly payroll processing, as the increased rate shall be applied when filling the annual Personal Income Tax declaration (form GPM311) and the subsequently calculated difference will have to be paid by the 1st of May of the following year. Even so, by agreement between the employer and the employee, the progressive PIT rate of 32 % can be applied and deducted by the employer every month, thus reducing the contributions that the employee would need to transfer to the tax authority after the end of the year. For all that, it is important to note that even if the latter method is chosen and applied, the taxpayer who received the income is still responsible for the correct calculation and payment of PIT to the tax authority since all income received during the year is assessed, not only that received from the current employer.

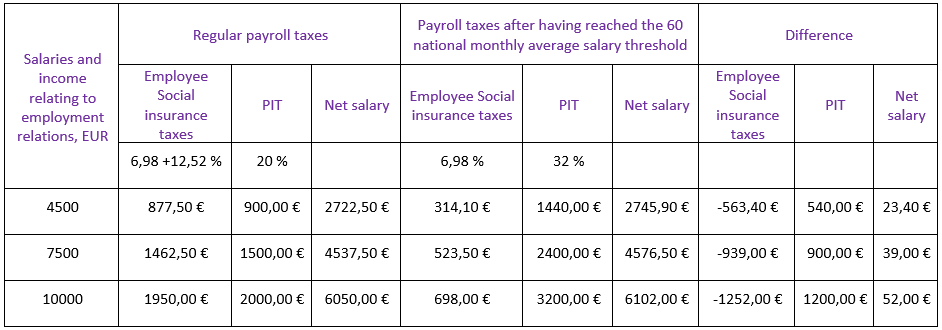

Please find an example below showcasing the differences between tax rates and the taxation of income earned within different income levels:

It should be noted that changes in tax rates only apply from the time the income threshold is reached until the end of the calendar year. From 1st of January of the following year, the standard payroll tax rates apply again until the threshold of 60 national monthly average salaries is reached.

* salary income, allowances or remuneration for activities in the supervisory board or board, loan committee, paid instead of royalties or together with royalties, income received from a person related to the taxpayer in employment relations or relations corresponding to their essence, according to copyright contracts, as well as the managers of small associations who are not members of those small associations according to the Law of the Republic of Lithuania on Small Associations, according to the civil (services) contract, income received for management activities).

-

Inesa Greičė Inesa Greičė - Grant Thornton Baltic UAB Partner | Head of Payroll Department

Inesa Greičė Inesa Greičė - Grant Thornton Baltic UAB Partner | Head of Payroll DepartmentView Profile